After years of rising premiums, growing deductibles, and expanding plan complexity, American consumers are showing signs of fatigue with the health insurance status quo. While many still rely on their plans and participate in employer-based systems without complaint, there’s a growing sense that insurance has become harder to use, more expensive to maintain, and less aligned with what people actually need. Health systems and insurers face an increasingly skeptical user base. One that’s asking not just what their plan covers, but why it costs what it does, and whether it’s worth it at all.

To better understand this shift, we used the third-party survey platform Pollfish to conduct a national survey of 600 insured adults, examining how people perceive the value of their current health plans, what they prioritize when choosing coverage, and where frustrations most often emerge. The findings are revealing, not just because of what consumers say, but because of the tension between their stated satisfaction and their actual behavior.

Most respondents report feeling reasonably content with their coverage. They rate their plans as good or excellent and express confidence that their insurance would support them through a major health issue. But this surface-level satisfaction doesn’t tell the full story. Many are avoiding care due to out-of-pocket costs, struggling to understand what’s included in their coverage, and questioning whether today’s health plans offer the same value they did even five years ago. Nearly everyone is willing to consider trading benefits for savings.

This report unpacks those findings and explores what they mean for health systems working to stay relevant, trusted, and responsive. What emerges is a clear mandate: coverage must do more than check boxes. It must deliver clarity, control, and care that feels accessible and worth the investment. Anything less will continue to erode the fragile trust consumers place in the system.

The Illusion of Satisfaction

On the surface, Americans appear relatively content with their health insurance. They describe their plans as “good” or even “excellent.” They express confidence that their coverage would support them in the face of a major medical issue. But the moment the conversation shifts to cost, that confidence begins to crack.

When presented with the option of trading away benefits for lower premiums, more than 80% of respondents say they’d at least consider it. Nearly a third are ready to make the switch outright. This is a remarkable signal of discontent, especially from a group that had described their plans in mostly positive terms. The takeaway is clear. People aren’t loyal to their coverage; they’re loyal to what they can afford. When forced to choose between benefits and price, affordability nearly always wins.

This paradox, feeling satisfied while being ready to jump ship, speaks to a broader challenge facing health systems. For many, their current plan is simply “good enough,” not because it works perfectly, but because the alternatives feel equally flawed. Consumers are compromising by default, not choosing with conviction.

Implication: Health plans must stop confusing inertia with loyalty. Consumers want streamlined options that meet their most important needs without bloated extras or financial unpredictability. Offering modular, transparent plan structures could help people feel empowered by their coverage rather than trapped by it.

The Cost of Care You’re Already Paying For

One of the most unsettling patterns to emerge from the survey is that many people are actively avoiding care even when that care is covered. More than half of respondents say they’ve skipped a procedure, appointment, or prescription because of out-of-pocket costs, despite the service being included in their plan.

Affordability may be top of mind, but the data indicates that there’s also a pervasive lack of confidence in the system. People aren’t sure what their plan will actually pay for, or how much they’ll owe once the bill arrives. That uncertainty is powerful enough to override medical need. Clarity, not coverage, is the real issue.

When patients are making decisions about their health based on financial anxiety rather than medical advice, something has gone wrong. The core purpose of insurance is to make care more accessible, not less. Yet the psychological weight of unpredictable expenses is pushing people away from care they’ve technically already bought.

Implication: Clear, real-time communication about costs and coverage should be table stakes. Health systems have the opportunity to provide this clarity by working directly with employers to provide coverage for their employees. This allows health systems to keep more patients within their existing hospital and provider networks and prevent fragmented and confusing care.

Value Is a Moving Target and It’s Moving in the Wrong Direction

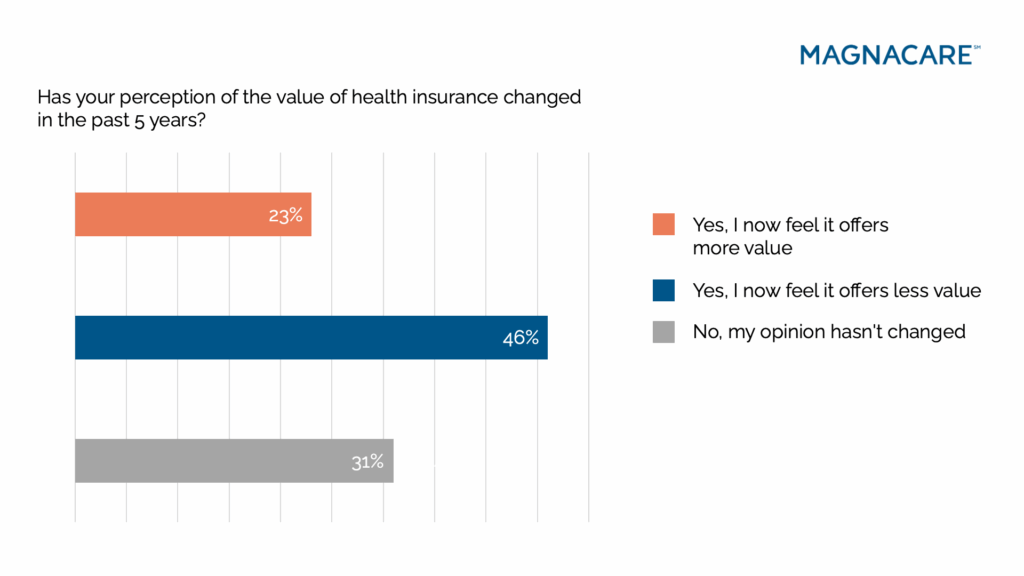

For nearly half of respondents, health insurance feels worse than it did five years ago. They aren’t just dissatisfied with today’s costs, they believe they’re paying more and getting less. This isn’t a quiet complaint, but a shift in cultural mindset.

Even among those who rated their insurance as “good,” this perception of declining value holds strong. Half of all those respondents said their plan has lost value in the last five years, and that number goes up the lower people ranked their plan’s value. This suggests that the baseline expectations for insurance have changed. It’s no longer enough for a plan to simply exist. It needs to feel worth the price tag.

Consumers are looking at rising premiums, growing deductibles, narrower networks, and slower access and deciding that the math no longer works in their favor. They want a system that feels fair, modern, and designed with their needs in mind.

Implication: As consumers see declining value from insurers, health systems can step in with an alternative. By providing healthcare coverage directly to employers and bypassing traditional insurance carriers, they can improve the value of key areas like preventative care access, wait times, and provider quality.

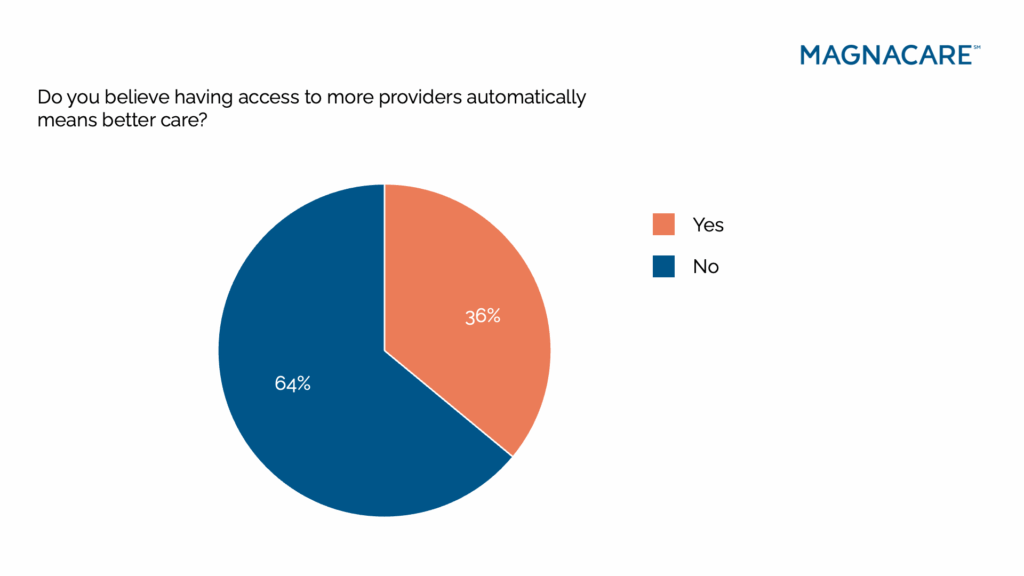

What People Want Isn’t More Options, But Better Ones

One of the clearest themes to emerge from the survey is that consumers are done equating “more” with “better.” While most people say they prefer plans that offer a large number of covered services, they don’t believe a bigger provider network necessarily means higher-quality care. In fact, the more bloated and complex a plan feels, the less confidence people seem to have in it.

This reveals an important shift in mindset: Breadth without clarity is no longer appealing. Consumers don’t want to feel like they’re navigating a maze of options or choosing from a buffet of benefits they may never use. They want their healthcare to be curated and designed around access to the right providers, not just more of them. They want faster answers, fewer tradeoffs, and smarter coverage. They want meaningful access to trustworthy care. This can’t happen under the current insurance-based model, where patients get fragmented care and their various doctors and health systems don’t communicate with one another.

Implication: Patients want more streamlined care. Health systems can address their frustrations by providing an alternative to the status quo: the direct-to-employer model. With all of their doctors in the same system, patients don’t have to navigate the in-network/out-of-network maze. Plus, the health system benefits by increasing domestic utilization and revenue.

The findings from this survey reflect a health insurance system that, while functionally intact, is losing ground in the eyes of its users. Most people aren’t walking away from their health plans, but are questioning their value, avoiding care, and preparing to trade away coverage if it means greater affordability. These are signals of compromise, not confidence.

Consumers are navigating their plans with hesitation. They feel the weight of financial unpredictability, struggle to decode what’s included, and often choose not to use the care they’re entitled to. At the same time, they express a strong desire for control over costs, access to providers, and understanding of their options. They aren’t asking for more. They’re asking for better, simpler, clearer.

This growing disconnect between coverage and perceived value presents an opportunity for health systems to realign how plans are structured, communicated, and delivered. Closing that gap doesn’t necessarily require a sweeping transformation. What it requires is closely listening and designing around what people actually need, not just what regulations or market norms dictate.

Key Takeaways for Health Systems

- Satisfaction is not loyalty.

People may say they’re content with their coverage, but the moment a lower-cost option is presented, even with fewer benefits, they’re willing to consider it. Default enrollment and auto-renewals may be masking deeper dissatisfaction. - Perceived value is trending downward.

Nearly half of consumers feel insurance offers less value than it did five years ago. That’s a sentiment problem, and sentiment drives consumer behavior more than spreadsheets do. - Lack of affordability is driving avoidance.

Over half of respondents are skipping care that’s covered because of out-of-pocket costs. This means that, on top of pricing, communication is a serious issue. When costs feel opaque or unpredictable, people disengage. - Clarity is the new currency.

Two-thirds of respondents feel overwhelmed by what their plan does or doesn’t cover. Simplifying the user experience, both through clearer documentation and intuitive tools, should be a strategic priority. - Consumers want curated access, not bloated networks.

A bigger list of providers isn’t solving the problem. People want to see trusted doctors, within the same health system, quickly and easily. That means investing in navigation, not just expansion. - Preventive and mental health care are rising expectations.

From coverage of screenings to mental health services, consumers are demanding plans that prioritize long-term wellness, not just emergency intervention. - Trust is built on transparency, speed, and follow-through.

Consumers don’t expect perfection. They expect honesty, predictability, and the ability to resolve issues without entering a bureaucratic maze.

Ultimately, the path forward lies in making healthcare less fragmented and easier to use. The direct-to-employer model can overcome common challenges patients are facing by removing friction, anticipating needs, and meeting consumers where they are, not where the system assumes they should be. By giving patients greater clarity into what’s covered and where they can access care, health systems can offer the value that many feel is missing from their current coverage.

This approach eliminates the hurdles and confusion that often deter patients from seeking care. In addressing these common barriers, health systems can build patient loyalty and establish a more reliable revenue stream. Everyone benefits when the system realigns around what matters most: meeting the short- and long-term needs of patients.